Introduction

Enterprise AI adoption has reached widespread levels, yet most organizations remain unable to extract measurable value from their investments. According to Boston Consulting Group, 74 percent of companies struggle to achieve and scale value from AI initiatives, while research from MIT indicates that 95 percent of generative AI pilots fail to deliver return on investment. This analysis examines the structural factors behind these failures, with particular attention to the domain gap problem in regulated industries and the phenomenon known as "pilot purgatory." The evidence suggests that implementation challenges stem primarily from organizational and process factors rather than technical limitations, and that domain-specific AI solutions will increasingly displace general-purpose models in enterprise contexts.

The Scale of Implementation Failure

The gap between AI experimentation and scaled business impact has widened considerably. Industry statistics indicate that the average enterprise scrapped 46 percent of AI proof-of-concepts before reaching production, up from 17 percent the previous year. Research on scaling challenges shows that nearly two-thirds of companies report being stuck in pilot phases, unable to transition to full operational deployment.

This phenomenon, commonly referred to as "pilot purgatory" or the "GenAI Divide," reflects a fundamental disconnect between boardroom expectations and operational reality. While executive optimism remains high, IBM's analysis reveals that most enterprise-wide AI initiatives have yielded only a modest 5.9 percent average return. McKinsey's Global Survey 2025 confirms that although AI tools are now commonplace, only 39 percent of organizations report any earnings impact from AI at the enterprise level.

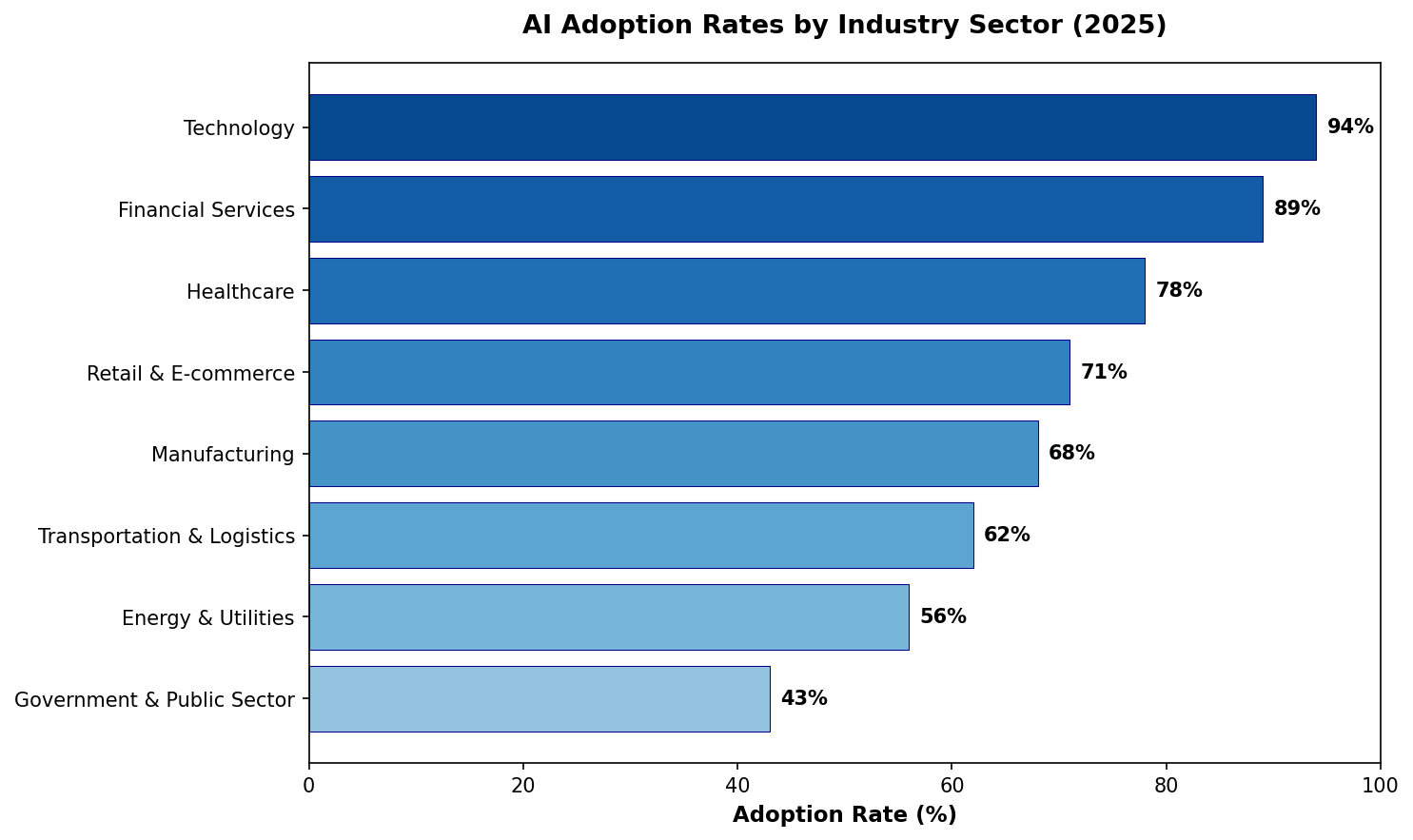

AI Adoption Rates by Industry Sector (2025) - Regulated industries lag behind technology sector

AI Adoption Rates by Industry Sector (2025) - Regulated industries lag behind technology sector

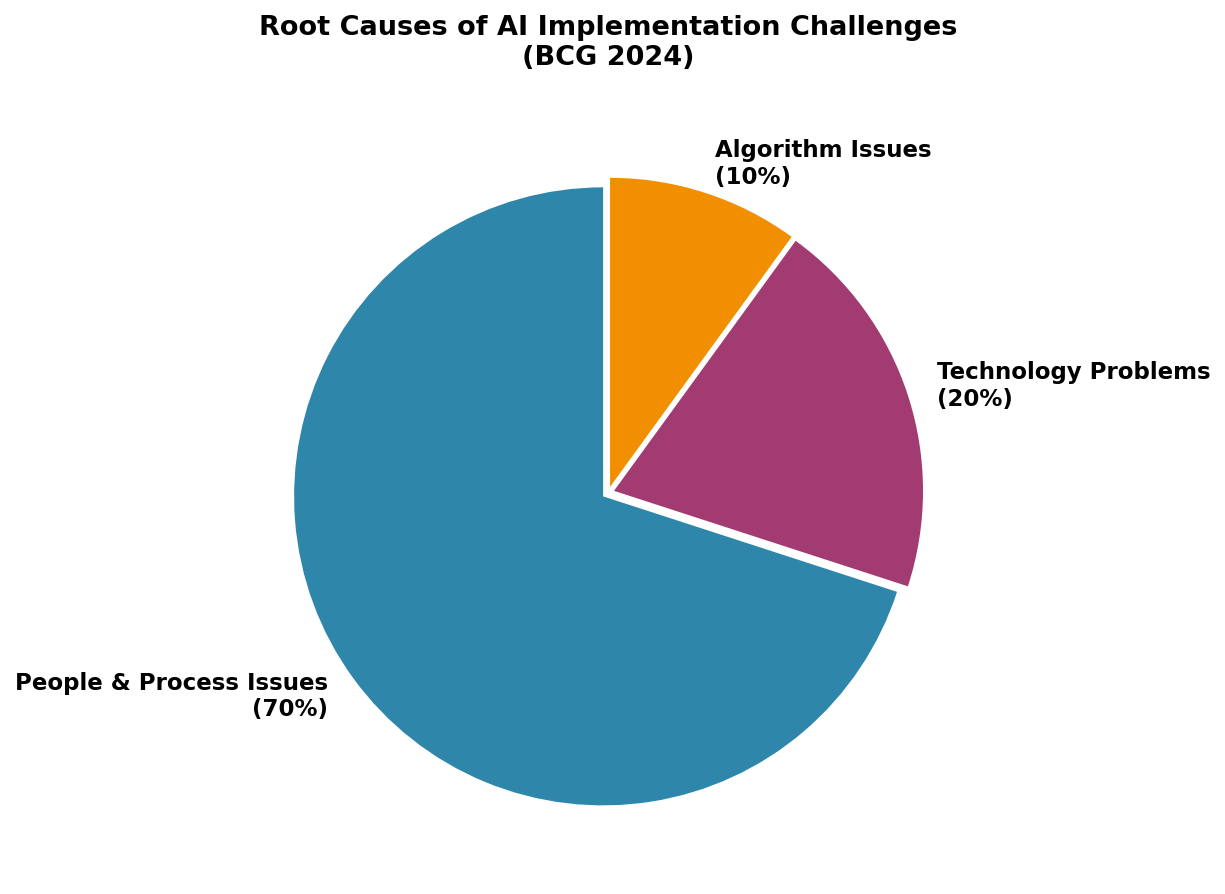

The root causes of these failures are instructive. Research from Boston Consulting Group indicates that approximately 70 percent of AI implementation challenges originate from people and process issues, 20 percent from technology problems, and only 10 percent from algorithm-related factors. This distribution suggests that organizations are allocating disproportionate attention to technical optimization while neglecting the organizational changes necessary for successful deployment.

Root Causes of AI Implementation Challenges (BCG 2024)

Root Causes of AI Implementation Challenges (BCG 2024)

The Domain Gap: Why General-Purpose AI Struggles in Specialized Contexts

General-purpose large language models demonstrate flexibility that makes them effective for individual productivity tasks, but they encounter significant limitations in enterprise workflows. Analysis of the GenAI Divide identifies the core issue: these models do not learn from, adapt to, or retain feedback from specific organizational contexts. They function as pattern-recognition systems predicting linguistic sequences rather than knowledge repositories capable of distinguishing factual accuracy from plausible-sounding output.

This limitation becomes acute in domains requiring precision and expert judgment. Research on domain-specific AI notes that in healthcare applications, language models must comprehend medical terminologies, diagnoses, treatment protocols, and drug interactions. Without domain-specific training, these systems struggle with complex medical concepts and may produce dangerous misinterpretations. Legal and financial contexts present similar challenges, where general AI typically generates overly broad or inaccurate information that fails to meet professional standards.

The performance differential between general and domain-specific AI is substantial. Enterprise AI analysis shows that specialized models trained on curated, industry-relevant datasets consistently outperform general-purpose alternatives in focused applications. They also require fewer computational resources, making them more cost-effective for targeted use cases. Market research from Technavio projects that the global vertical AI market will grow by 126.6 billion dollars from 2025 to 2029, expanding at a compound annual growth rate of 24.3 percent.

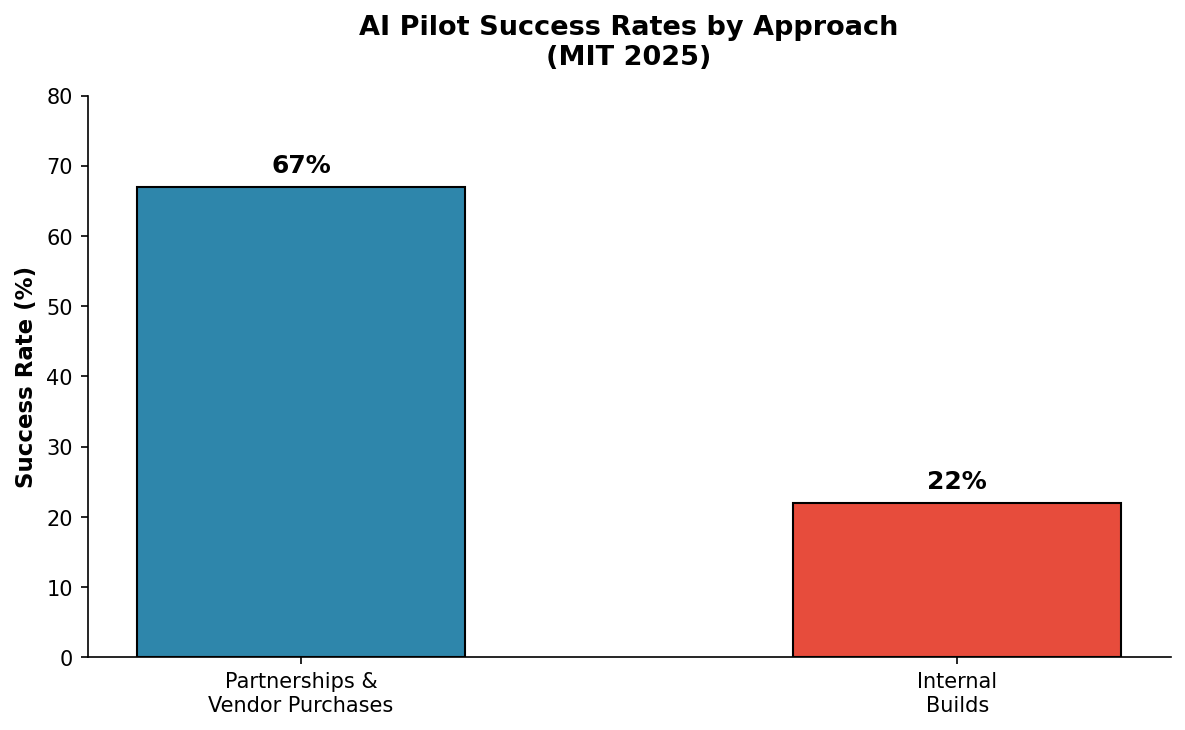

AI Pilot Success Rates: Partnership vs Internal Build Approaches (MIT 2025)

AI Pilot Success Rates: Partnership vs Internal Build Approaches (MIT 2025)

Regulated Industries: Structural Barriers to Adoption

The adoption gap between technology companies and regulated sectors reflects fundamental architectural differences in how these organizations can approach AI deployment. Industry analysis notes that technology firms can adopt cloud-based AI solutions and validate security measures reactively. Financial services, healthcare, aerospace, and government entities cannot operate this way; they require solutions that meet compliance requirements before deployment.

In healthcare, comparative analysis of AI adoption shows that compliance with privacy regulations contributes to annual costs exceeding 39 billion dollars. Healthcare transformation research indicates that only 16 percent of healthcare organizations have implemented system-wide AI governance frameworks, and more than 80 percent of hospitals have not adopted AI in any meaningful capacity. Public trust presents an additional barrier: surveys indicate that only 11 percent of adults are willing to share health data with technology companies, compared to 72 percent who feel comfortable sharing with physicians.

Financial services face similar constraints. Sector analysis reveals that in one regional market, only 9 percent of financial institutions identify themselves as AI leaders, largely due to regulatory uncertainty. Research on enterprise AI barriers notes that the opacity of many AI systems, which make decisions through processes that are difficult to explain or audit, creates major obstacles for organizations required to justify automated decision-making under regulatory frameworks.

Several high-profile failures illustrate these challenges. A detailed case study documents how a major technology company invested approximately four billion dollars in an oncology AI system marketed for cancer treatment recommendations. The system's knowledge base, however, was heavily influenced by a single institution's practices, producing recommendations that frequently failed to align with local guidelines or drug availability in other regions. Similarly, analysis of AI failures found that a healthcare coverage algorithm had a 90 percent error rate when patients appealed its denial decisions, as the model failed to account for comorbidities and individual patient complexity.

Outlook for 2026: Domain Specialization and Measured Adoption

Industry forecasts suggest several developments in the coming year. The shift from general to vertical AI will accelerate, with market projections indicating global enterprise spending on domain-specific solutions will reach 47 billion dollars by 2030, growing at a compound annual growth rate of 40 percent. Analysis of AI trends suggests domain-specific small language models will transition from experimental tools to core components of enterprise AI infrastructure.

Deloitte's TMT Predictions 2026 projects the autonomous AI agent market will reach 8.5 billion dollars by 2026. However, spending rationalization is also expected, with Forrester predicting that enterprises will delay 25 percent of planned AI spending into 2027 as organizations demand clearer connections between AI investment and measurable business outcomes.

MIT research indicates that companies purchasing AI tools from specialized vendors and forming partnerships succeed approximately 67 percent of the time, while internal development efforts succeed only about 22 percent of the time. This finding suggests that 2026 will see increased emphasis on AI partnerships rather than proprietary development, particularly in regulated sectors where domain expertise and compliance knowledge are essential.

Regulatory expansion will further shape adoption patterns. Gartner's strategic predictions indicate that fragmented AI regulations are expected to cover half the global economy by 2027, driving approximately five billion dollars in compliance spending. This regulatory environment will favor specialized, compliant AI solutions over general-purpose alternatives that require extensive adaptation to meet sector-specific requirements.

Conclusion

The evidence demonstrates that enterprise AI success depends less on model sophistication and more on organizational readiness, domain expertise, and strategic integration with existing business processes. The high failure rate of AI pilots reflects structural factors—misaligned expectations, inadequate governance, and insufficient attention to workflow redesign—rather than fundamental technical limitations.

For practitioners in regulated industries, the path forward involves prioritizing domain-specific solutions that incorporate sector knowledge from initial design rather than attempting to adapt general-purpose tools after deployment. Organizations that address the learning gap, invest in appropriate governance frameworks, and redesign workflows rather than simply adding AI capabilities to existing processes will be better positioned to realize the productivity gains that AI theoretically offers.

This article was published on November 25, 2025.

References

- Boston Consulting Group: AI Adoption in 2024

- Fortune / MIT: State of AI in Business 2025

- McKinsey & Company: The State of AI Global Survey 2025

- IBM: How to Maximize ROI on AI in 2025

- Technavio: Vertical AI Market Analysis 2025-2029

- Deloitte: TMT Predictions 2026

- Forrester: Predictions 2026

- Gartner: Strategic Predictions for IT Leaders 2026